Understanding Pet Insurance: Navigating Coverage Options and Benefits

Pet insurance is the fastest-growing corner of the personal-lines insurance market in North America, and it is also the corner with the least consumer understanding. The category crossed a meaningful threshold in 2024: North American written premium hit $5.2 billion (+20.8% year-over-year), with 7.03 million insured pets (+12.2%) per the North American Pet Health Insurance Association's 2025 State of the Industry report. The average accident-and-illness premium for a dog runs $62.44 per month in 2025 — up roughly 11% in a single year — and $32.21 per month for a cat. Most policyholders never read the contract.

This guide is written from a consumer-journalist position. The phrase that matters most in pet insurance is pre-existing condition, the second is waiting period, the third is reimbursement schedule, and most claim denials trace back to one underlined clause the owner did not read when their puppy was eight weeks old. What follows is the fine print, with named carriers, current dollar figures, and the specific questions to ask before you sign.

How Pet Insurance Actually Works in 2026

US pet insurance operates almost entirely as reimbursement insurance, not direct-pay. The owner pays the veterinarian at the time of care, files a claim with itemised invoice and medical records, and receives a reimbursement after the deductible is met and the policy's reimbursement percentage is applied. Two carriers — Trupanion and a few specialty programs — offer direct-vet-pay options at participating clinics, but the dominant model remains pay-and-claim.

A 2026 policy quote in the US typically structures around three plan types:

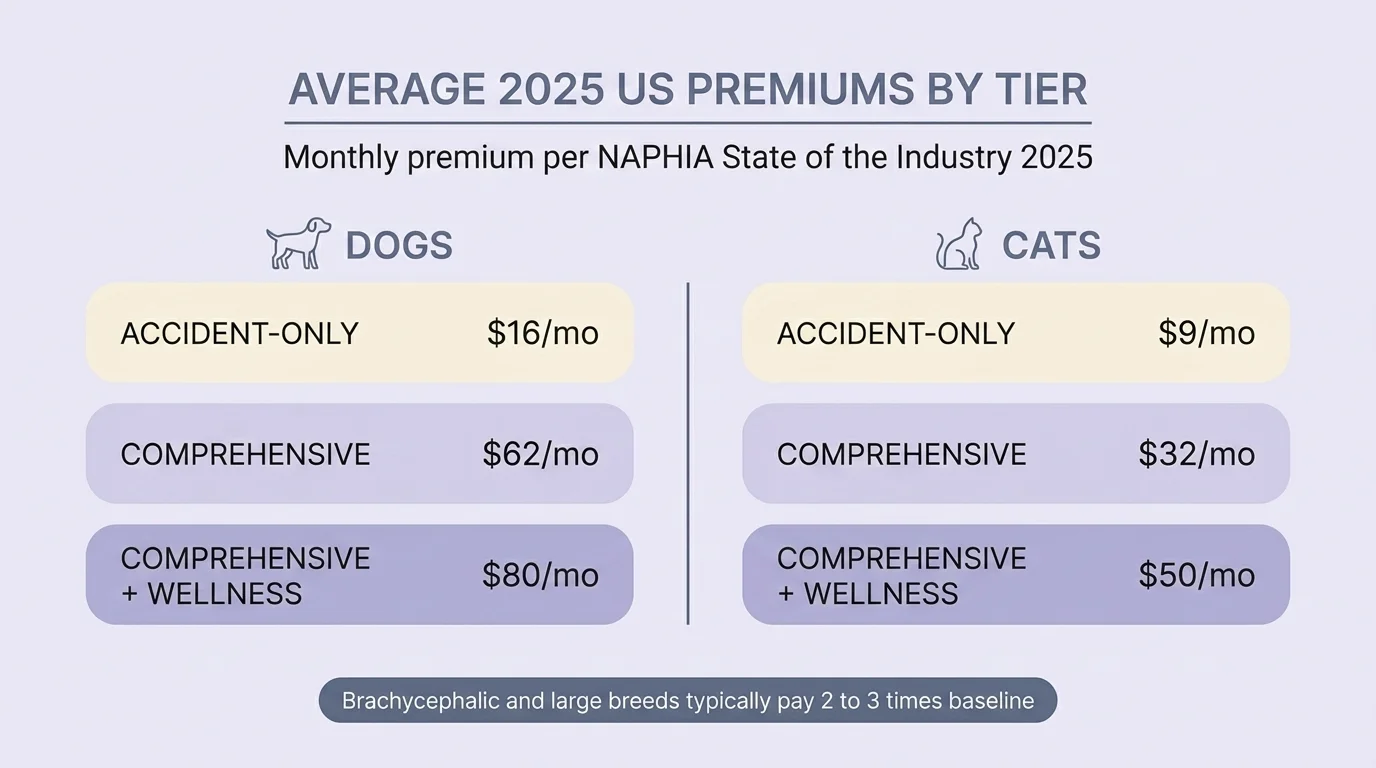

- Accident-only. Covers veterinary costs from accidents (broken bones, lacerations, foreign-body ingestion, toxin exposure). The cheapest tier — NAPHIA's 2025 average is $16.10/month for dogs and $9.17/month for cats. Excludes illnesses entirely.

- Accident-and-illness (comprehensive). Covers accidents plus illnesses (cancer, allergies, diabetes, infections, chronic conditions). The dominant US tier and the basis of most premium quotes — NAPHIA's 2025 averages of $62.44/month for dogs and $32.21/month for cats refer to this tier.

- Wellness add-on (optional rider). $10–$30 per month additional, covering routine care: vaccines, dental cleanings, flea/tick prevention, annual exams. Usually structured as a fixed annual benefit per category rather than a percentage reimbursement.

The terminology "time-limited" and "maximum-benefit" is largely UK-pet-insurance vocabulary and is mostly absent from the 2026 US market — most US comprehensive policies operate as annual-benefit-cap structures (with a few carriers, notably Trupanion, offering no-payout-cap structures at higher premiums).

The reader's first decision, in plain language: do you want catastrophic-event protection (accident-only or accident-and-illness with a high deductible and 70% reimbursement), or do you want comprehensive coverage including the smaller annual costs (accident-and-illness with a lower deductible, 90% reimbursement, and a wellness rider)? The first runs $16–$30/month for many dogs; the second runs $80–$130/month. Both are defensible decisions; the math is what differs.

Is Pet Insurance Worth It? The 10-Year Math

This is the question 9,900 people search every month, and most of the SERP avoids answering it. The honest answer is that pet insurance is arithmetically negative-EV for the average pet, the way auto insurance and homeowners' insurance are negative-EV for the average household. Insurance companies are profitable because the average policyholder pays more in premiums than they receive in claims. Pet insurance is mathematically excellent against catastrophic events, where a single $10,000 emergency surgery can trigger years of premiums in a single visit.

Three lifetime worked examples:

A healthy mixed-breed Lab, enrolled at 1 year old, comprehensive plan. Premium ≈ $50/month, rising ~5–8% annually with age. Ten-year premium total ≈ $7,500. Expected claims for a healthy mid-size mixed breed ≈ $3,500–$5,500 over the same period (one or two minor accidents, occasional infections, end-of-life care). Net cost: roughly $2,000–$4,000 over 10 years for catastrophic-event protection. If the dog gets a $7,000 cruciate surgery in year five, the math flips dramatically in the policyholder's favour.

A French Bulldog, enrolled at 1 year old, comprehensive plan. Premium ≈ $130/month, rising similarly with age — French Bulldogs and English Bulldogs generate 2–3× baseline claim frequency for brachycephalic respiratory, dental, and skin conditions. Ten-year premium total ≈ $19,500. Expected claims often exceed $15,000 over the same period. Net cost is closer to break-even for a Frenchie, and the variance is so wide (a single BOAS surgery is $4,000–$8,000) that the catastrophic-event case is unusually strong for high-claim breeds.

A senior dog, enrolled at age 8. Premium starts at $100+/month and rises faster. Five-year horizon. Pre-existing exclusions limit what is covered. Many comprehensive plans become net-negative for the owner unless they specifically choose a carrier that covers curable pre-existing conditions after a symptom-free period (see below). Senior enrollment is the hardest case — owners often discover that the conditions they most want covered are the ones excluded.

The principled framing: pet insurance is a catastrophic-event hedge, not a savings vehicle. If you can self-insure $5,000–$10,000 in unexpected vet bills without financial stress, the case weakens. If you cannot — and most households cannot — it is high-value.

Pre-Existing Conditions: What's Actually Covered

This is the section that decides more enrollment regret than any other. Pre-existing condition in pet insurance contracts means a medical condition that existed, was diagnosed, or showed clinical signs before the policy effective date or during the waiting period. Carriers vary widely on:

- Whether the lookback to find pre-existing conditions is 14 days, 30 days, 6 months, 12 months, or the pet's entire history (most use full medical history).

- Whether curable pre-existing conditions can be re-covered after a symptom-free period.

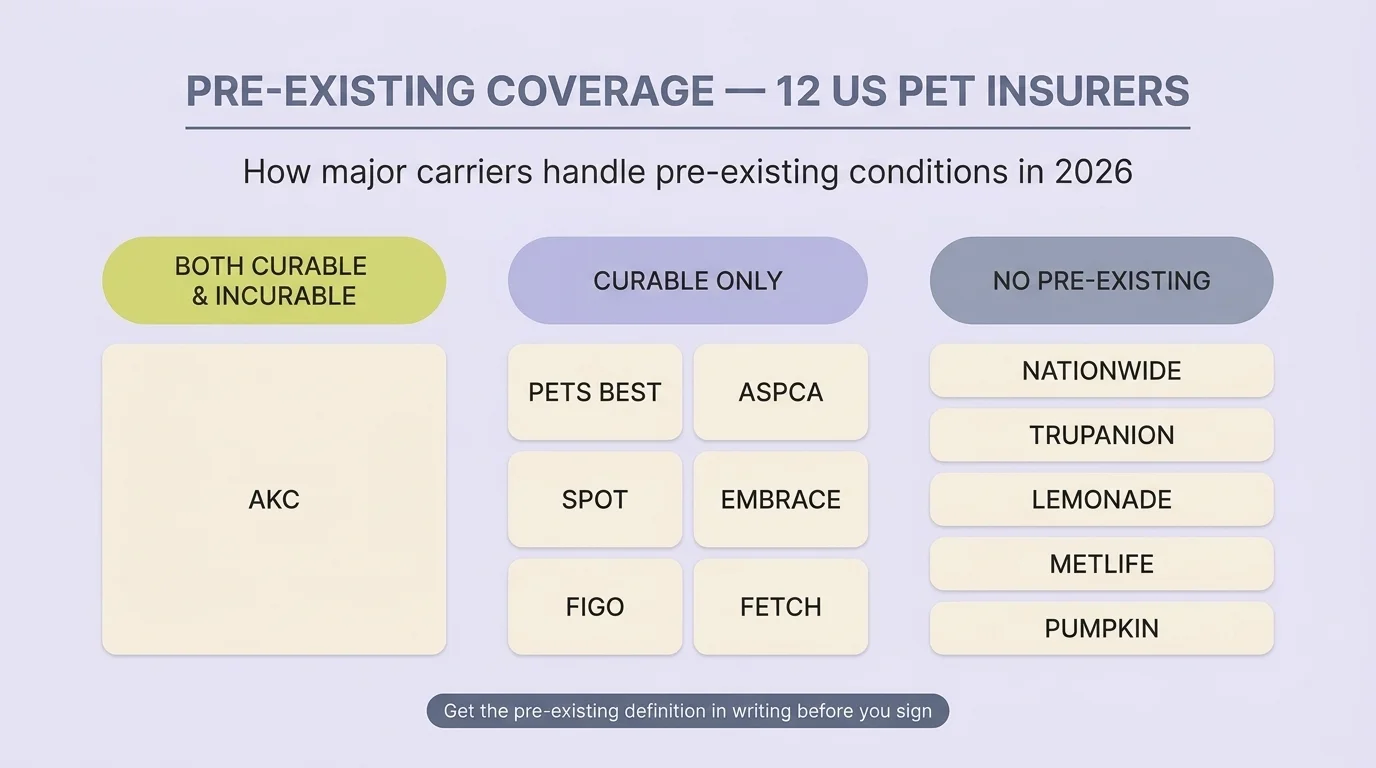

- Whether incurable pre-existing conditions can ever be covered (rarely; AKC is a notable exception).

The 2025–2026 carrier landscape, from carrier policy documents:

| Carrier | Curable pre-existing covered? | Symptom-free period | Notable exclusion |

|---|---|---|---|

| AKC Pet Insurance | Both curable AND incurable | 365 days continuous coverage; 180 days for IVDD/cruciate | Most-generous policy in the US market |

| Pets Best | Curable only | 180 days symptom-free | Examples: broken bones, sprains, URIs, dental fractures |

| ASPCA | Curable only | 180 days symptom-free | Knee/ligament conditions excluded |

| Spot | Curable only | 180 days symptom-free, no professional treatment in window | Knee/ligament conditions excluded |

| Figo | Curable only | 12 months cured | — |

| Fetch | Curable only | 12 months symptom-free from policy start | — |

| Embrace | Curable only | 12 months symptom-free | — |

| Nationwide | No | — | All pre-existing permanently excluded |

| Trupanion | No | — | All pre-existing permanently excluded |

| Healthy Paws (legacy; now Embrace book) | No | — | New enrollments route to Embrace |

| Lemonade | No | — | All pre-existing permanently excluded |

| MetLife | No | — | All pre-existing permanently excluded |

| Pumpkin | No | — | All pre-existing permanently excluded |

The single largest factual error in the consumer SERP is that AKC's #1-ranked pre-existing-conditions page implies they are uniquely able to cover pre-existing conditions. That is technically true for incurable conditions; for curable conditions, six other major carriers (Pets Best, ASPCA, Spot, Figo, Fetch, Embrace) cover them after a defined symptom-free or cured period. Buyers comparing carriers should know the distinction.

A practical rule: if your pet already has a chronic condition (allergies, mild arthritis, recurring ear infections), AKC is the only major US carrier that meaningfully covers ongoing care for that condition. If the condition is curable (a broken bone that healed, a treated UTI, a one-off skin infection), six carriers cover it after the symptom-free window. If you are enrolling a healthy young pet, the pre-existing question matters less today and more in two to three years — choose a carrier with a generous curable-pre-existing policy as a hedge.

The Three Levers: Deductibles, Reimbursement, and Waiting Periods

Once you have selected a carrier and a plan tier, three levers determine what the policy actually pays out and when:

Deductible

Most US pet insurance plans use an annual deductible ($100, $250, $500, $750, or $1,000 are typical tiers), reset each policy year. A few carriers offer per-incident deductibles instead, which favour healthy pets with occasional acute events. A higher deductible lowers the premium meaningfully — moving from $250 to $750 typically reduces the premium by 15–30% — at the cost of more out-of-pocket exposure on smaller claims.

Reimbursement Percentage

After the deductible is met, the policy pays a fixed percentage of approved claims. Standard tiers: 70%, 80%, or 90%. A 90% plan with a $250 deductible on a $5,000 cruciate ligament surgery returns $4,275 to the owner ($5,000 – $250 = $4,750 × 90% = $4,275); a 70% plan with a $750 deductible returns $2,975 on the same surgery. The reimbursement and deductible together determine the realised payout, and the math compounds across multiple claims in a year.

A few carriers (notably Trupanion) operate on a co-insurance model with no per-incident or annual cap, paying 90% of approved claims regardless of total. Trupanion premiums are correspondingly higher; the model is excellent for large-breed dogs prone to chronic conditions and expensive specialty care.

Waiting Periods

The waiting period is the time between policy effective date and when coverage starts. Industry-standard:

- Accidents: 48 hours (some carriers: immediate or 24 hours).

- Illnesses: 14 days (some carriers: 30 days).

- Orthopaedic and cruciate ligament conditions: 6 months (Embrace, Pets Best, others). Some carriers (Hartville, MetLife) offer no orthopaedic waiting period, which materially matters for breeds at high cruciate risk.

Anything diagnosed during the waiting period is treated as pre-existing — even if the policy is in effect. This is the fine-print clause most-cited in claim denials. The practical lesson: enrol when the pet is healthy, not when symptoms appear.

What's Actually Covered (and What Isn't)

A 2026 comprehensive accident-and-illness policy from a reputable US carrier typically includes:

- Accidents and emergencies (foreign-body surgeries, fracture repairs, toxin treatments).

- Illnesses, acute and chronic (cancer, diabetes, allergies, kidney disease, IBD).

- Hereditary and congenital conditions — now baseline coverage across Embrace, Healthy Paws, Spot, ASPCA, Trupanion, Pets Best, Figo, Lemonade if not symptomatic before enrolment. The original framing that "hereditary conditions may be excluded" is dated and now applies primarily to budget-tier or accident-only plans.

- Diagnostic testing, prescriptions, hospitalisation, surgery, specialist consultations.

- Behavioural therapy and alternative therapies — covered as standard by Embrace, Spot, ASPCA, Pets Best, Figo; some carriers require an add-on rider.

What is typically excluded:

- Pre-existing conditions as defined above.

- Routine and preventive care unless purchased via wellness rider.

- Elective and cosmetic procedures (declawing, tail docking, ear cropping where legal, anal-gland expression in some plans).

- Breeding-related care (breeding, whelping, complications related to intentional breeding).

- Experimental or investigational treatments (some plans cover with vet documentation; most exclude by default).

- Boarding, grooming, food and supplements (with limited exceptions for prescription diets in some plans).

Wellness Plans: When the Add-On Pencils Out

A wellness rider runs $10–$30/month additional. It typically reimburses a fixed annual amount per category — for example, $50/year for dental cleaning, $25/year per vaccine, $50/year for flea/tick prevention. The math is straightforward: add up what you actually spend on routine care annually, subtract the rider's annual premium, and see whether you are net-positive.

For most healthy young pets on a standard wellness schedule, the rider is roughly break-even, plus or minus $50/year. The break-even improves for households that diligently use every benefit category (dental cleaning, all vaccines, parasite prevention, annual exam) and worsens for households that skip categories. The non-financial argument for the rider — that it reduces the friction of paying for preventive care and increases owner uptake of preventive services — is real, and is one of the few cases where a roughly break-even insurance product is still defensible. For senior pets, where dental and bloodwork volume rises, the rider often pencils out clearly positive.

The Claims Process and Why 18% of Claims Get Denied

The reassuring number first: a 2025 MarketWatch industry survey found 82% of pet insurance policyholders reported zero issues during the claims process — a higher satisfaction rate than human health insurance.

The other 18% follows five predictable patterns, in declining frequency (Bankrate, ManyPets, Money 2025 reports):

- Pre-existing conditions — the largest single denial category. Symptoms documented in vet records before the policy effective date or during the waiting period. Mitigation: get 12 months of vet records before applying, ask the carrier in writing to identify any conditions they would consider pre-existing, and document anything ambiguous before signing.

- Missed filing deadlines — most carriers require submission within 90–180 days of treatment; late claims are auto-denied. Mitigation: file claims weekly or biweekly, not after a year of accumulated invoices.

- Insufficient documentation — itemised invoice plus 12 months of medical records is the modern standard. Missing diagnostic notes or a vet letter is the most-fixable cause of denial; most carriers will pay on resubmission with the missing document.

- Waiting period claims — accidents in the first 48 hours, illnesses in the first 14–30 days, orthopaedic in the first 6 months. Mitigation: do not file claims for events during a known waiting period; they will be denied and may be flagged as pre-existing for future events.

- Services excluded by policy — routine dental cleanings without a wellness rider, elective procedures, breeding-related care, cosmetic procedures. Mitigation: read the exclusions section before signing; circle anything that applies to your pet's likely future.

The single biggest mitigation, in plain English: enrol when your pet is healthy and document everything. Most denials are predictable from the application process forward; very few are surprises that the policyholder could not have anticipated by reading the contract.

How Much Does Pet Insurance Cost? The 2026 Picture

The headline numbers from NAPHIA's 2025 State of the Industry report and PetMD's cost analysis:

| Coverage type | Dogs (2025 avg) | Cats (2025 avg) |

|---|---|---|

| Accident-and-illness comprehensive | $62.44/month ($749.29/year) | $32.21/month ($386.47/year) |

| Accident-only | $16.10/month | $9.17/month |

| Wellness add-on (rider) | typically +$10–$30/month | typically +$10–$30/month |

Premium drivers:

- Age. Premiums rise meaningfully with each year, accelerating after age 7. A senior dog enrolling at age 8 may pay double a 2-year-old enrolment.

- Breed. French Bulldogs, English Bulldogs, Bernese Mountain Dogs, Great Danes, Cavalier King Charles Spaniels typically pay 2–3× baseline for brachycephalic, hereditary cardiac, or short-life-span health profiles. Mixed-breed dogs and domestic shorthair cats run at or below baseline.

- ZIP code. Vet costs in major metropolitan areas (NYC, San Francisco, Boston, LA) drive premiums 30–60% above national averages.

- Deductible and reimbursement choice. A $750 deductible and 70% reimbursement plan can be 30–40% cheaper than a $250 deductible and 90% reimbursement plan on the same pet.

- Spay/neuter status. Some carriers offer modest discounts for spayed/neutered pets.

The 2025 11% dog-premium increase year-over-year tracks veterinary cost inflation specifically — emergency and specialty veterinary services are up 30%+ in some metros since 2022 per AVMA cost-of-care data, driven by board-certified specialists, expanded MRI/CT availability, and reinsurance market hardening.

Choosing a Carrier: 7 Questions to Ask Before You Sign

Wirecutter, Forbes Advisor, and NerdWallet all run useful annual best-of rankings. Rankings shift; the questions to ask do not. Use this checklist on every quote you receive:

- What is the pre-existing condition definition, and is the lookback the pet's full history or a defined window? Get this in writing.

- What are the waiting periods, by category — accident, illness, orthopaedic, cruciate? A six-month orthopaedic waiting period materially matters for breeds at risk; carriers that waive it are worth the slightly higher premium for the right pet.

- What is the benefit cap structure — annual, per-incident, or unlimited (no payout cap)? Trupanion is the major no-cap option in the US; most others are annual-cap structures at $5,000, $10,000, $15,000, or unlimited.

- How does the reimbursement schedule actually work? Some carriers reimburse based on a benefit schedule (a fixed table of "this much for this procedure") rather than a percentage of the actual invoice. Schedule-based reimbursement frequently underpays; percentage-based reimbursement is the modern standard.

- What is the rate-increase history and policy? Premiums rise with age and inflation; some carriers cap year-over-year increases, most don't. Ask for actual rate-increase history for similar pets in your ZIP code over the past five years.

- What are the cancellation terms? Some carriers refund unused premium; some don't. Cancelling mid-year on a chronic-illness diagnosis is a particularly painful situation if the policy doesn't return prorated premium.

- Is the carrier compliant with California SB 1217 disclosure requirements (relevant to all carriers, since the standard is becoming national)? An "Insurer Disclosure of Important Policy Provisions" document delivered with the quote in 12-point type is now table-stakes.

Independent of the rankings, the 2026 top-tier US carrier shortlist most reviewers agree on: ASPCA (best overall), Spot (best perks/multi-pet), MetLife (best multi-pet, no upper-age limit), Pumpkin (fastest claim turnaround), Embrace (best customisation), Lemonade (cheapest baseline), Trupanion (no payout caps), and AKC (best pre-existing conditions). The right choice depends on the answers to the seven questions above as applied to your specific pet.

What's Changed Since 2024: Consolidation and California SB 1217

Two structural changes since the original publication of this piece deserve flagging.

Carrier consolidation. Chubb acquired Healthy Paws in 2024, and in 2025 Embrace Pet Insurance acquired Healthy Paws' policy portfolio, effectively absorbing one of the most-recommended carriers of the prior decade into Embrace's book. Existing Healthy Paws policies continue under Embrace's administration; new enrolments now route to Embrace directly. Most articles older than six months still treat Healthy Paws as an independent flagship — if you are reading a "best pet insurance" comparison that lists Healthy Paws as a separate option, the comparison is stale.

California SB 1217. Effective January 1, 2025, under California Insurance Code § 12880.2, every pet insurer offering policies in California is required to:

- Produce a standalone "Insurer Disclosure of Important Policy Provisions" document in 12-point or larger type, delivered with the policy and posted on the insurer's homepage.

- Disclose if premiums increase based on the pet's age.

- Disclose if premiums increase based on geographic relocation.

- Disclose whether a medical exam is required to start coverage.

- Disclose all waiting periods explicitly.

- Disclose all exclusions explicitly.

The NAIC's Regulator's Guide to Pet Insurance is the inter-state model law California's reform draws on, and similar bills are in committee in New York and Washington as of early 2026. The practical takeaway for buyers anywhere: a carrier that cannot or will not provide a clear disclosure document is a compliance red flag and a reasonable basis to walk away. A carrier that provides one — even outside California — is signalling the kind of transparency that correlates with cleaner claims processes.

Pet Insurance for Specific Life Stages

Puppies and kittens. The strongest case for early enrolment is the absence of pre-existing conditions to exclude. A 2-month-old puppy enrolled before any medical history accumulates locks in coverage for hereditary and congenital conditions that would otherwise become exclusions later. Premiums are also at their lowest. The downside: most claim activity in the first two years is minor (vaccinations, parasite checks, minor accidents) and reimbursement may not yet exceed premiums paid. The math improves over the policy's lifetime.

Senior pets. Enrolment after age 7 is harder. Many carriers have upper age limits (Healthy Paws / Embrace traditionally cut off new enrolment at 14 for accident-and-illness; MetLife is one of the few with no upper age limit). Pre-existing exclusions hit hardest at this stage. The carriers worth considering for senior enrolment: MetLife, AKC, Embrace, Pets Best, Spot — and specifically the carriers that cover curable pre-existing conditions after a symptom-free period if the senior pet has any history.

Exotic pets. Nationwide remains the dominant US carrier for exotic species (birds, reptiles, rabbits, small mammals); Embrace added limited exotics in 2024; most other US carriers still decline. Premiums for exotics are higher per-month and benefit caps are typically lower; the case is strongest for high-value exotics (parrots, large reptiles) where a single illness can produce vet bills that outpace the lifetime premium cost.

A Brief Closing Note

The honest position on pet insurance: it is a useful financial product for most households that cannot self-insure $5,000–$10,000 in unexpected vet bills, and it becomes a high-value product the moment a pet faces a single catastrophic event. The category has matured meaningfully in the past five years, with hereditary conditions now baseline coverage, behavioural therapy increasingly included, pre-existing rules genuinely improving for curable conditions, and California's SB 1217 raising the disclosure floor for every carrier doing business there.

The same caution that applied a decade ago still applies. Read the exclusions section before signing. Get the pre-existing condition definition in writing. Document the pet's medical history before the application date, not after. Never assume a claim will be covered without the contract language to back it up. The 82% of policyholders who report no claim issues are the ones who did the homework upfront. The 18% who get denied are mostly the ones whose policy did exactly what it said it would do — they just hadn't read it.

For specific decisions — which carrier is right for your pet, which deductible/reimbursement combination matches your budget and risk tolerance, whether to enrol now or wait — talk to your veterinarian (they see what gets denied), an independent insurance agent (they can compare carriers without a vested interest in one), and your own household budget. This guide is the framework. The contract you sign is the medicine.

Last reviewed 2026-04-29 by Nisha Chandran.

Frequently Asked Questions

Pet insurance is arithmetically negative-EV for the average pet — most policyholders pay more in premiums than they receive in claims. It is mathematically excellent against catastrophic events: a single $7,000 cruciate surgery or $10,000 cancer treatment can flip the math dramatically in the policyholder's favour. The principled framing is that pet insurance is a catastrophic-event hedge, not a savings vehicle. If you can self-insure $5,000–$10,000 in unexpected vet bills without financial stress, the case weakens. If you cannot — and most households cannot — it is high-value, particularly for high-claim breeds like French Bulldogs and Bernese Mountain Dogs.

A medical condition that existed, was diagnosed, or showed clinical signs before the policy effective date or during the waiting period. Carriers vary on whether the lookback uses 14 days, 30 days, 6 months, 12 months, or the pet's full history (most use full history). Curable pre-existing conditions can be re-covered after a symptom-free period (180 days at Pets Best/ASPCA/Spot; 12 months at Embrace/Figo/Fetch). Incurable pre-existing conditions are permanently excluded by most carriers — AKC Pet Insurance is the major US exception, covering both curable and incurable pre-existing conditions after 365 days of continuous coverage.

Per NAPHIA's 2025 State of the Industry report, the US average comprehensive accident-and-illness premium is $62.44/month for dogs ($749.29/year) and $32.21/month for cats ($386.47/year). Accident-only is dramatically cheaper at $16.10/month for dogs and $9.17/month for cats. Wellness add-ons run $10–$30/month additional. Dog premiums rose ~11% in 2025 alone. Brachycephalic and large-breed dogs (French Bulldogs, English Bulldogs, Bernese Mountain Dogs, Great Danes) typically pay 2–3× baseline due to higher claim frequency.

Yes — but with important distinctions. AKC Pet Insurance is the only major US carrier covering both curable AND incurable pre-existing conditions after 365 days of continuous coverage (180 days for IVDD/cruciate). Six other major carriers cover curable pre-existing conditions only, after a symptom-free period: Pets Best, ASPCA, and Spot at 180 days; Embrace, Figo, and Fetch at 12 months. Nationwide, Trupanion, Lemonade, MetLife, and Pumpkin do not cover any pre-existing conditions. The distinction between curable and incurable is critical — most chronic conditions (diabetes, allergies, kidney disease) are incurable and only AKC covers them.

Industry-standard waiting periods: 48 hours for accidents (some carriers immediate or 24 hours), 14 days for illnesses (some carriers 30 days), and 6 months for orthopaedic and cruciate ligament conditions. Hartville and MetLife are notable exceptions that waive the orthopaedic waiting period. Conditions diagnosed during a waiting period are treated as pre-existing — even if the policy is in effect — which is the fine-print clause most-cited in claim denials. Enrol when your pet is healthy, not when symptoms appear.

About 82% of pet insurance claims process without issues per a 2025 MarketWatch industry survey. The 18% denial rate follows five predictable patterns: (1) pre-existing conditions — symptoms documented before the policy effective date or during the waiting period; (2) missed filing deadlines — most carriers require submission within 90–180 days; (3) insufficient documentation — itemised invoice plus 12 months of medical records is the modern standard; (4) waiting period claims — accidents in the first 48 hours, illnesses in the first 14–30 days, orthopaedic in the first 6 months; (5) services excluded by policy — routine dental cleanings without a wellness rider, elective procedures, breeding-related care. Most denials are predictable from the application process forward and are mitigable by reading the contract before signing.